Limited company or Sole Trader?

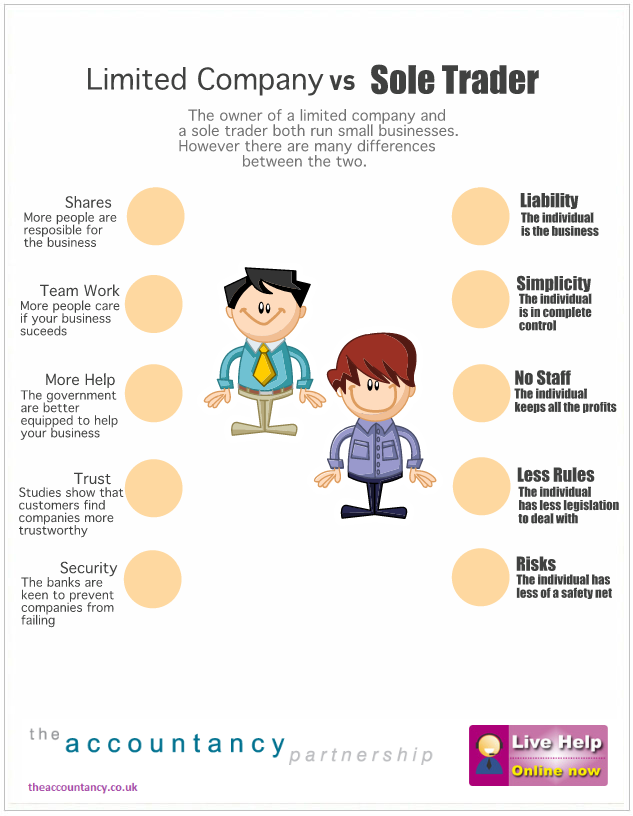

The Accountancy Partnership has put together an infographic showing the difference between Limited Companies and Sole Traders in a cute but informative way.

The Accountancy Partnership has put together an infographic showing the difference between Limited Companies and Sole Traders in a cute but informative way.

Limited companies and sole traders are two of the most popular business models for small companies. Even though both models can provide similar services and products for their customers there are distinct pros and cons for each.

Sole Traders have the joy of being in complete control of their business. With nobody else to answer to, sole traders can get things done quickly and efficiently; this means no business opportunities are missed due to meetings or administrative tasks. Sole traders also have less legal boundaries than limited companies and this offers a lot more freedom about what information they make public with regards to their business. Sole traders also see 100% of the profit their business makes because they have no shareholders or permanent staff. Unfortunately sole traders are subject to some of the highest tax rates of any business. Sole traders also have very few options if their business fails as they are entirely financially responsible; meaning their personal assets could be at risk if they owe creditors.

Limited Companies are far more risk free. There will be a team of shareholders with a vested interest in the company and this means your company is more likely to succeed. Limited companies are also more likely to get financing from banks, business angels and private investors as they appear more official and, in turn, more trustworthy. Limited companies also have various tax breaks available to them that sole traders do not have access to; meaning the percentage of tax they pay is far less. There are some disadvantages to limited company status though. Limited companies have to share a lot of information, including profits and share prices, publicly; if your company has had a bad year this can be a PR disaster.

Choosing which of these business models is best for your small business is tricky. If your business is small enough to be operated alone then sole trading is perhaps the best option as you are not bogged down by bureaucracy in your early years. That said, if your business is becoming too successful to handle on your own, limited company status is easy to obtain if you need it. If you need further advice seek consultation from a financial advisor or small business accountant.

Infographic on behalf of The Accountancy Partnership

Delicious

Delicious Digg

Digg StumbleUpon

StumbleUpon Propeller

Propeller Reddit

Reddit Magnoliacom

Magnoliacom Newsvine

NewsvineSocial Tracking

![]()

![]()

![]()

![]()

Comments

Post new comment